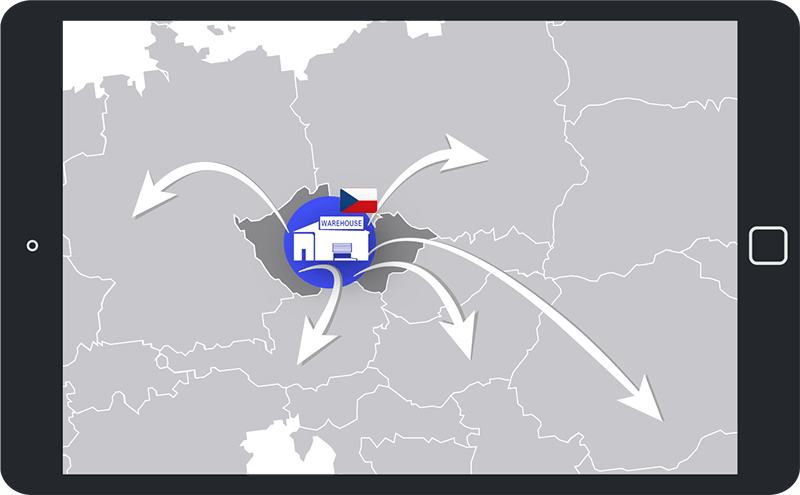

Storing stock in a Czech warehouse rented from a 3PL fulfillment provider triggers the obligation to register for VAT in Czechia. It's advisable to complete your registration before sending your stock to avoid customs clearance issues and import VAT reclaims.

For sellers utilizing Amazon FBA, it's important to understand the different FBA programmes and their VAT implications. Amazon's FBA programmes include:

Choose one country for stock storage, requiring registration in that country (e.g., Spain).

Choose multiple countries for stock storage, necessitating immediate VAT registration in the selected countries.

Distribute stock across up to 8 countries, including Spain. Register for VAT in all 8 Amazon FBA Pan European countries.

Let SimpleVAT manage the complexities of VAT registration, filing, and OSS/IOSS registration for your e-commerce business. Our expert team ensures compliance with Czech tax regulations, allowing you to focus on scaling your business. Contact us today to discover more and embark on your journey!